How Much Do I Need for Early Retirement?

My Goal: Freedom 35

People often tell me that my travel goals are crazy but, in many ways, my goals for early retirement are even crazier.

Being raised and educated in Canada, I was always encouraged to obtain a university education, find a secure career, claw my way up the corporate ladder, and prepare to retire 40 years later. That’s when, in theory, I would finally have time for traveling, hobbies, reading, golfing, and generally enjoying my life.

I’m not a patient person. My goal is to compress 40 years of working into less than 15 years and reach retirement (or financial independence) by the ripe age of 35.

While my Freedom 35 plan is essentially an early retirement plan, I prefer to say my goal is achieving Financial Independence since I cannot see myself as your stereotypical retiree. To me, early retirement means giving up work entirely, playing bingo Wednesday nights, seniors’ golf tournaments, and taking lots of naps.

While early retirement may be great for some, the idea of Financial Independence appeals to me far more. Let me explain why…

What is Financial Independence?

My interpretation of financial independence, or Findependence, is having sufficient personal wealth to live without having to work actively for basic necessities. In other words, I would like my assets to generate income that is greater than my expenses which will give me the benefit of CHOOSING what I do every day rather than being FORCED to work for money.

Financial independence is having sufficient personal wealth to live without having to work actively for basic necessities.

I like to challenge myself intellectually and physically on a continual basis and need to have a sense of purpose in life. Studies show that happiness is actually derived from having control over events in our lives rather than money. That is why financial independence appeals to me so much.

I believe it is important to always challenge myself and those challenges may present themselves in a variety of forms. Once I haveFindependence I may still choose to take another job, start-up an entrepreneurial venture, work on a creative personal project, or focus on a self-improvement goal. The key is that I will have CHOICE and CONTROL over what I pursue and when I pursue it.

The biggest problem with achieving financial independence or early retirement is knowing when you have saved enough to actually pull the trigger and quit your job!

Why Financial Advisors Suck

I tend to disagree with most retirement advice I read such as:

- You will earn 5-6% investment returns after inflation during your saving years;

- You will spend 70-80% of your pre-retirement income in retirement;

- You can withdraw 4% of your retirement savings each year (the 4% rule); and

- You need to save 10x your pre-retirement income to retire.

While these assumptions are based on historical returns and sound calculations to an extent, the assumptions are based on people with typical saving habits, historical returns, poor spending habits, and little investment knowledge who don’t plan to retire until their 60s. Clearly, such assumptions will not apply to me, a traveling nomad who wants to retire at 35.

Financial advisors also often act as salespeople, pushing products and investment strategies that they will gain compensation from rather than the products that are actually the best for you. Mutual funds are a rip-off yet lots of people still buy them. Why? Financial advisors tell them to or their company savings schemes force them to.

Okay, so if Financial Advisors suck, you can just use an online Financial Calculator to make your own calculations right? Not so fast…

Why Financial Calculators Suck

Most financial calculators are also based on absurd fixed rates and assumptions. After you input your current age, income, and savings the rest of the variables are based on your best guesses: assumed retirement age, assumed savings rate, expected annual raises or increases in income, assumed life expectancy, assumed retirement spending, assumed inflation rate, assumed social security benefits, and assumed investment returns. These numbers are often fixed which does not reflect reality since equity returns, fixed income rates, and inflation changes every year!

Any retirement or financial independence calculations are going to require assumptions to a certain extent, but I have come up with a conservative mathematical methodology, based on actual historical events, that gives me a clear understanding of my ability to actually become Financially Independent at 35.

The Better Way of Calculating Financial Needs

The biggest problem with trying to become financially independent at 35 is that so much can go wrong between 35 and whenever I die. If I live until I’m 95 that means I will face 60 years of potential recessions, depressions, and inflation crises. Even though I expect to die around 85 given my love for beer, travel, crazy adventures, and risky activities, there is also a strong possibility that medical advancements over the next 60 years will allow me to reach 100+.

As discussed above, most financial advisors and calculators use assumptions like 7% stock market returns and 2% inflation rates to make their calculations. The calculator I use actually tells me how my retirement strategy would have performed based on actual US stock market performance since 1871.

The benefit of using this calculator is that it calculates if my retirement would succeed if I invested my retirement savings at the absolute worst time (height of the largest stock market bubble) or at the absolute best moment in over 100 years. While investing at the best possible time would mean lots of excess returns, I am more interested in seeing the worst-case scenario since that indicates whether I am able to proceed with my Freedom 35 plans or not.

There are a lots of variables and assumptions that you can make in the calculator but for my purposes I can assume I will have no debts, social security, or pension income; inflation will be in-line with historical CPI; and my annual spending will remain consistent as I age (though I fully expect I’ll spend less money and more time napping as I age).

Given how long I expect to be retired, I am also comfortable with investing 85% of my portfolio in equities versus fixed income with a 0.18% management fee, the rate charged by many ETF Index funds.

After plugging all of this into the FireCalc, I have a great idea of what I will need to retire and the best and worst case financial scenarios I can expect based on historical US market returns.

How Much Do I Need for Freedom 35?

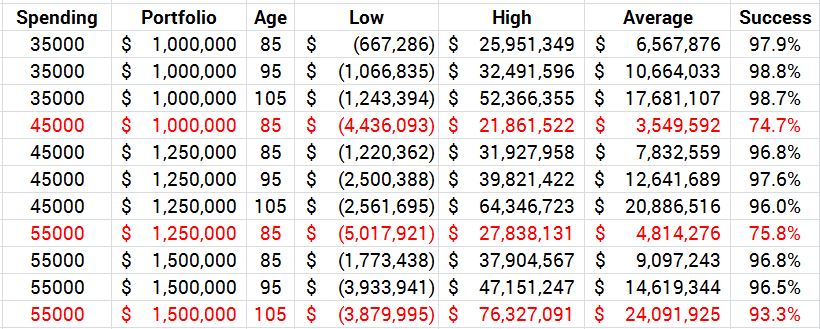

I know I cannot predict my retirement spending or age of death with exact precision so I made a table to compare and model a variety of potential retirement outcomes.

Starting with a spending level of $35,000 per year and a retirement portfolio of $1,000,000, I wanted to see what my chances of successfully retiring at 35 and living until 85, 95, or 105 were. Good news is that the success rates were all greater than 97%.

Next, I wanted to know if I could bump my annual spending up to $45,000 per year and still succeed. Unfortunately, with a retirement portfolio of only $1,000,000, the expected success rate is less than 75%, but if I retire with a starting portfolio of $1,250,000 the chances for success increases to over 96%.

Similarly, if I want to spend $55,000 per year for the rest of my life, I will need to have around $1,500,000 in my portfolio for high probabilities of success.

Freedom 35 Financial Independence Model Results

I like seeing these results visually presented as it shows that my spending levels have a far greater impact on my retirement portfolio requirements than my life expectancy. It is also nice to see how great my retirement could be if my portfolio performs on average or better! Obviously, my portfolio could not drop below zero unless someone allowed me to borrow ridiculously but the low value also shows how harsh market bubbles can be!

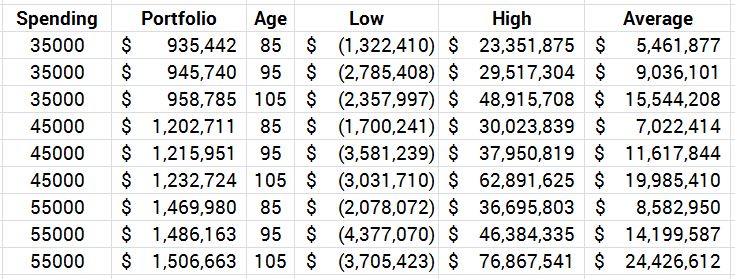

Another way to model this is to determine an acceptable success rate % and determine the required retirement portfolio investment amount that way. In my opinion, a 95% success level is more than reasonable given it is extremely unlikely I will invest my entire retirement portfolio in equities at the height of a market bubble. I then conducted an analysis using the same annual expenditure and age of death values as in the table above:

Freedom 35 Portfolio Requirements Based on 95% Success Rate

Based on these results, if I plan to spend $35,000 per year I only need ~$950k in retirement savings whereas spending $55,000 per year would require a retirement portfolio of ~$1.5 million.

So… How Much Do I Need for Early Retirement?

For the last decade of traveling, I have sought to spend less than $100 per day on average. In 2015, my total expenses were less than $30k and I lived a very good lifestyle without being frugal. If you don’t believe me, check out my year in review. I actually believe the $30k I spent in 2015 is significantly more than I would spend if I traveled less, rented accommodation by the month instead of the day, and cooked for myself instead of regularly eating out.

The problem with using $30k as my base spending requirement is that I was not spending any money to maintain a home or car in 2015. Eventually, I do want to settle down somewhere and while I can exclude the purchase cost of my home from my portfolio’s capital requirement quite easily, the ongoing utility, maintenance, and taxes could easily add $5k/year to my living expenses.

Further, if I have a family I will need to ensure I have enough to support raising children, putting them through university, and going on family trips. The costs of children could easily surpass $10k/year but since I fully support minimalism and free-range parenting I can assure you my kids will not be spoiled with costly brand name clothing or electronics and instead enjoy the freedom of the great outdoors.

Based on these considerations, I believe a minimum annual income of $45k is a reasonable estimate for my income needs. Therefore, to ensure I succeed in reaching financial independence by 35, I will want a portfolio of around $1.25 million by the time I’m 35 to gain Financial Independence then.

You may scoff at $45k and think it is too low but remember this is the minimum amount I will be able to spend each year and still live off my investments. If the market performs well I could have a portfolio that grows to $30 million plus!

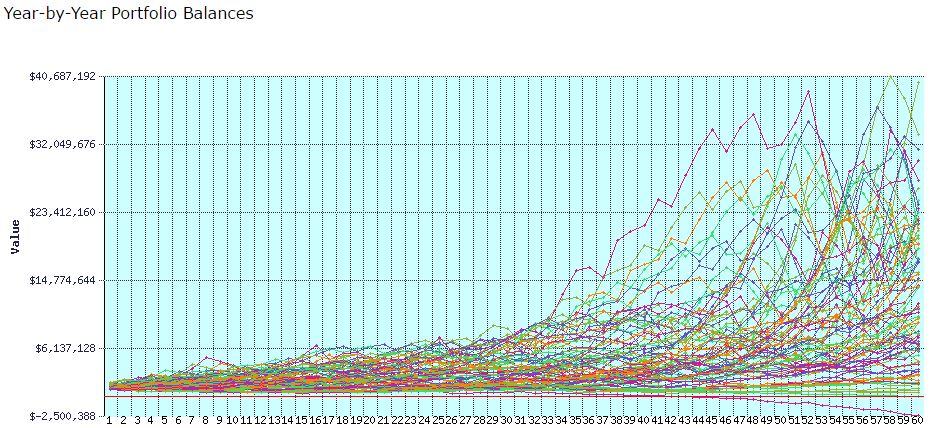

If you’re having a hard time understanding how my FireCalc model works, I’ve provided an example of this scenario below:

FireCalc Model: $1.25M Portfolio, $45k spending, Retire 35, Die 95

What the model shows is that over 85 historic periods, my retirement with $45k in annual expenditure would have succeeded 83 out of 85 times (97.6%). It also shows that my portfolio would have grown to an average of $12,641,689 with a maximum of $39,821,422 by the end of my retirement after accounting for CPI inflation. Of course, I don’t care how much money is left when I’m dead but I do like how many scenarios are reaching $4-6 million by the time I’d be in my early 60s.

Based on the above, I’m targeting saving $1.25 million, plus the additional capital I may want for a home or to start a hobby business in retirement.

What are your early retirement or financial independence targets? Let me know in the comments below!

Very inspiring post and goals. Have you achieved your financial independence yet? How did you do it? Is there another post to it?

Thanks! I did quit my job at the end of 2020 so I’ve enjoyed over 2 years of “retirement” already. In reality, I’ve stayed super busy moving to Spain, re-learning how to invest and the tax consequences (Spain is a bureaucratic nightmare) and getting started on numerous hobbies.

I’ve been trying to avoid spending too much time on my computer but eventually I will start updating the blog more, including posts on FIRE.

Nice. That sounds great. Hope we can see some updates and insights soon. I am wondering to retire asap as well. 😉

It’s refreshing to read your ideas and thoughts. I have similar goals.

Some of the things I’m uncertain about are the following:

-Do you have contingency plans in case of illness? Assuming you are living outside of North America and don’t have insurance (USA) or healthcare (Canada). Medicine and doctors can eat away your savings very quickly.

-What places are you considering to settle down in and raise a family? Many countries would be amazing to live in but the education system and opportunities for your children would be limited. Private schooling followed by University in North America would be ideal but its expensive. Any thoughts?

Thanks,

AJA

I have thought a lot about both of your points but do not necessarily have concrete plans.

1. I’ve generally been very healthy but I definitely need to think about the increased medical issues I’ll face in the future as I age. Last year, I purchased international medical insurance with a $10k deductible just because I was planning to spend so much time in the US and was worried about being bankrupted by a medical event. For most of my travels, I self-insure based on the unlikelihood I will face something major and fact that medical costs are so much lower in most parts of the world I travel to. Next year I’ll be living in Colombia which provides excellent health care for very affordable prices and I will likely just “pay as I go” in the event I have an issue. In general, there is going to be a trade-off between the access to public health care and the amount of taxes I pay so in many ways I’ll be paying for medical insurance one way or the other throughout my life. There is also a booming “medical tourism” industry in many countries including Thailand, much of Central America, and countries like Colombia so traveling for any non-urgent care is also a possibility.

2. I expect to end up in Spain with a few years back in Canada to raise a family, hopefully with some long (6-12 month) international adventures mixed in to raise multi-lingual children (English, Spanish, ????). I love the lifestyle in Spain and that’s where my partner is from so it makes sense to live there and the schools are generally quite good. I hope to have the time to do a lot of homeschooling myself and my girlfriend is a teacher which will also help ensure they receive quality education. I’ve never understood the point of having kids if you don’t have the time to spend on them and that’s one of the great benefits of Financial Independence / Early Retirement in my opinion. For University, there are a lot of wonderful options in Canada and Europe which are very cost effective but it will generally depend on my children’s goals in life and work interests. I see University becoming less and less relevant but will plan to help my children pay for it so they can graduate debt free. I used to work 250+ hours/month in the summer during University to pay for the schooling costs in Canada and will expect my kids to also learn the value of hard work and good financial habits.

I like the idea but saving over 1 million dollars by 25 seems like it’s impossible. Can you advise on how to do that?

Saving 1 million by 25 would be pretty tough unless you inherited a load of cash or started a business that grew incredibly quickly. My goal was to save a million by 30 following a more conventional path of studying at University and becoming a working professional. I will do a blog post on my tips for earning / saving money in the near future. Stay tuned…

So what will you do with all your free time once you retire in 4 years? Just curious.

There are hundreds of things I would like to have more time for which is why Freedom 35 is so important to me.

I definitely want to keep traveling. I´d also like to give back to the community through volunteering or other philanthropic pursuits.

Eventually, I want to build a home or cabin in the mountains with fruit trees and hiking, mountain biking, fishing, skiing, snowboarding, and/or surfing nearby. An attached woodworking shop and garden / greenhouse would be a bonus!

Basically, I just want to be able to do what I want, when I want 🙂